APR ed APY: che cosa sono?

Due semplici sigle che possono cambiare completamente le strategie di investimento in criptovalute: cosa sono APR ed APY? Scopriamolo!

Indice

Introduzione a APR ed APY

Investendo ci si imbatte frequentemente in due acronimi che possono provocare confusione: APR ed APY.

Il caos può ulteriormente aumentare nel mondo delle criptovalute, dove ai classici termini della finanza si sommano quelli derivanti dalla blockchain.

Ancor prima di leggere grafici o svolgere analisi fondamentali, l’investitore profittevole deve conoscere le basi. Infatti, sarebbe arduo sviluppare strategie vincenti ignorando il significato delle parole chiave di questo settore.

APR ed APY traggono in inganno non solo i meno esperti: talvolta, persone già navigate faticano a illustrarne la differenza.

C’è una buona notizia: è tutto più facile di quello che sembra.

Questa mini-guida eliminerà qualsiasi dubbio sulla differenza tra APR ed APY, aiutandoci inoltre a comprendere come calcolarli.

Che cos'è l'APR

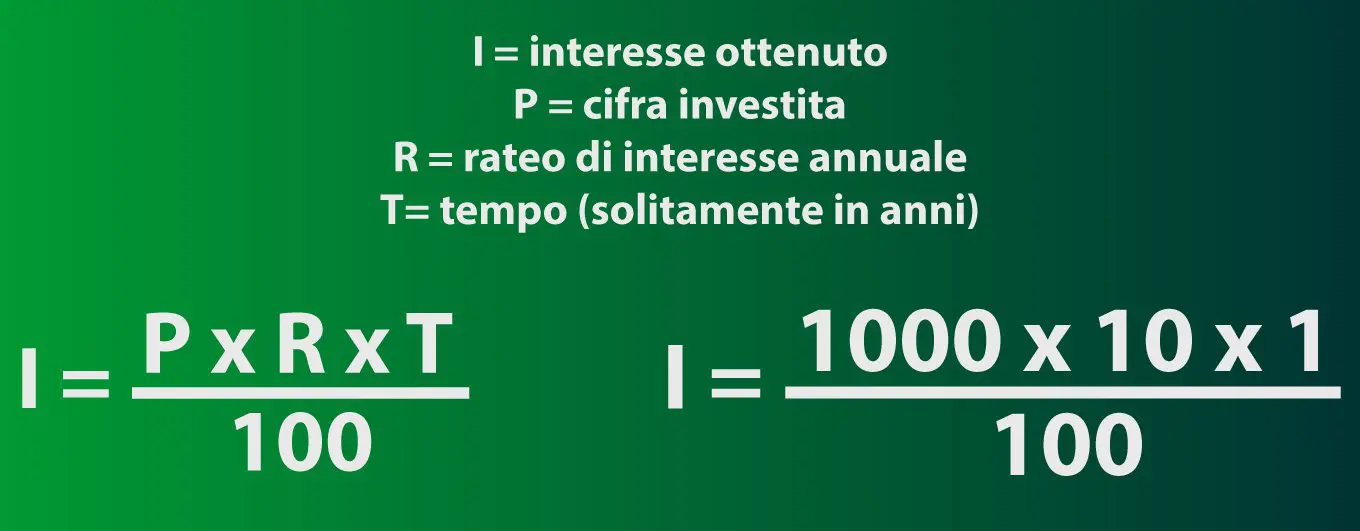

APR è l’abbreviazione di Annual Percentage Rate, cioè gli interessi che si ottengono annualmente dall’investimento. Si tratta di un dato semplice da calcolare in quanto non include l’interesse compound. Avvalendosi di un esempio sarà tutto più semplice da capire.

Immaginiamo di investire 1000€ in un prodotto che frutterà un APR del 10%.

Al termine del primo anno avremo guadagnato 100€, esattamente il 10% della somma impiegata.

Mantenendo collocata la stessa cifra, anche negli anni a venire otterremo sempre 100€.

L’APR è un dato basilare e che dipende esclusivamente dall’investimento iniziale. Infatti, il calcolo non prende in considerazione i guadagni generati con il passare del tempo.

A seguire troviamo formula e relativa applicazione ai dati impiegati nell’esempio.

Sorge una domanda: come poter calcolare gli interessi sul capitale sommato a quelli già ricevuti? Semplice: ricorrendo all’APY.

Che cos'è l'APY?

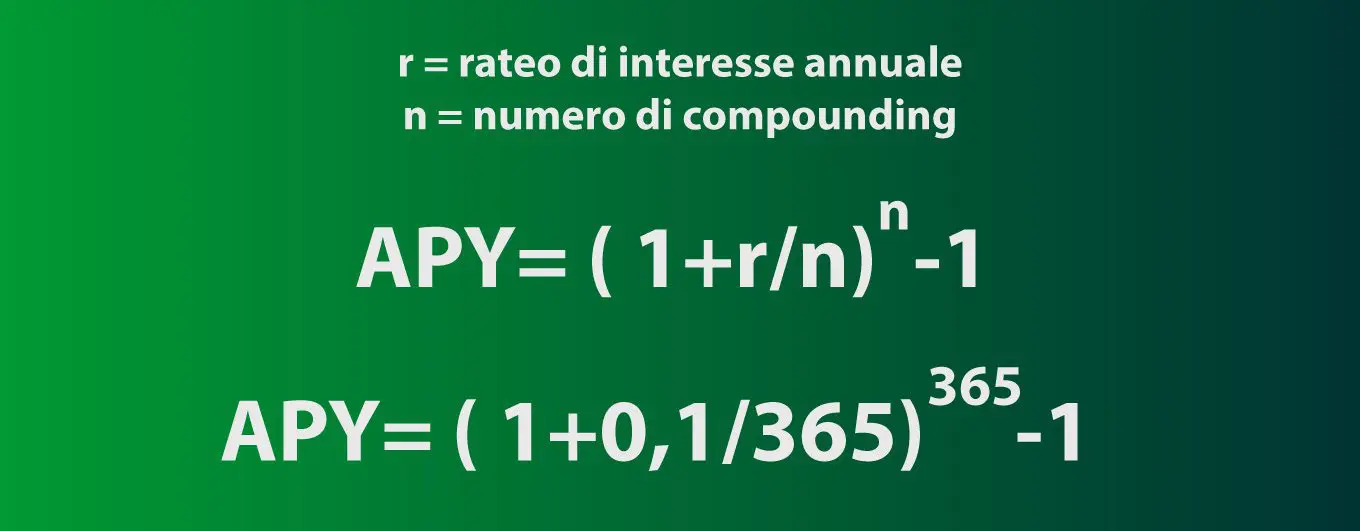

APY è l’acronimo di Annual Percentage Yield, ovvero il ritorno annuale di un investimento comprensivo dell’interesse compound. L’interesse compound consente di generare interessi sull’interesse, amplificando così i guadagni. Perdonate il gioco di parole, era impossibile da evitare .

Torniamo all’esempio portato con l’APR.

In quel caso, il 10% annuo non includeva alcun reinvestimento dell’interesse ottenuto. Al termine di ciascuna annualità, il ritorno sarebbe stato sempre lo stesso: 100€ sui 1000€ investiti inizialmente.

Supponiamo invece che ora si vada a tenere conto del compound.

Partiamo sempre con 1000€. Poniamo però che l’interesse venga pagato quotidianamente e in seguito reinvestito.

Al termine dell’annualità avremo ottenuto 1105,15€, con tasso effettivo del 10,5155% circa.

Più frequentemente viene erogato l’interesse compound, maggiore sarà il guadagno che andremo a ricevere.

Di seguito la formula e relativa applicazione ai dati utilizzati nell’esempio.

APR, APY e compounding nelle criptovalute

Investendo in criptovalute ci si imbatte di frequente in APR, APY e compounding. Dovremo ricordarci sempre questi punti:

- Quando la rendita viene indicata con l’APR, solitamente non è previsto il compound automatico. Saremo noi a dover raccogliere i frutti ottenuti e reinvestirli. L’aspetto positivo è che effettuando spesso quest’azione, l’interesse che andremo a riscuotere sarà superiore all’APR;

- Invece, nel caso dell’APY dovrebbe esserci una procedura autonoma che immette periodicamente la nostra rendita nel pool. La cifra corrispondente all’APY sarà esattamente quello che otterremo dopo un anno.

Ricorriamo a un esempio per fugare ogni dubbio: farm nel pool di liquidità ETH-USDC, rispettivamente coin di Ethereum e famosa stablecoin.

Se non vi fosse auto-compound, dovremmo procedere in questo modo:

- Raccogliere i token ottenuti;

- Eventualmente convertirli 50:50 in ETH e USDC. Questa è solitamente la prassi in quanto le rendite vengono spesso pagate in utility token;

- Versarli nel pool di liquidità in cambio di LP token;

- Depositare i token LP ottenuti nella rispettiva farm.

In presenza di auto-compound non sarà invece richiesta alcuna azione da parte nostra.

Anche nello staking si possono trovare processi automatizzati e non.

I tassi d’interesse possono inoltre esprimere anche il debito. Prendendo in prestito un asset su un dato protocollo, un NET APR negativo sarà l’interesse annuo da pagare, non a ricevere.

Se l’azione può tranquillamente essere condotta manualmente, ciò che davvero conta è verificare se l’interesse è espresso come APR o APY. In questo modo potremo fare correttamente tutte le nostre considerazioni e approfittare delle migliori opportunità disponibili.

Nota positiva: non occorre vivere con la calcolatrice in mano! Numerose piattaforme dispongono di calcolatori integrati e anche in rete ve ne sono un’infinità.

Conclusioni

Questo piccolo approfondimento volge al termine.

Prima di studiare incastri e strategie crypto complesse, le basi devono essere chiarissime.

APR ed APY fanno parte di questi pilastri: impossibile avere in mente numeri certi ignorando o confondendo questi dati.

Ci auguriamo che quanto appena scritto possa essere di aiuto per investire in criptovalute in maniera più sicura e consapevole.

Alla prossima!